The top end of the auction market has already made its choice.

Sotheby’s runs auctions through sothebys.com. Christie’s has built Christie’s LIVE into christies.com. Bonhams runs live and online-only sales through bonhams.com.

That is not just a matter of scale. It is a matter of strategy.

The leading houses understand that digital infrastructure is no longer just an operational tool. It is part of the business itself. It shapes how bidders experience the brand, how trust is built, how client relationships are retained, and how long-term commercial value is created.

A market that is still significant, but changing fast

The UK fine art, antiques and collectibles market remains one of the most important in the world. According to the Art Basel and UBS Global Art Market Report 2026, the UK remained the world’s second-largest art market in 2025, accounting for $10.5 billion in sales and an 18% share of the global market.

But it is also a market that is broader, more digital, and more competitive than it was even a few years ago.

For all the attention paid to marquee lots and high-profile evening sales, most auction activity happens far below the trophy end of the market. Art Basel’s 2025 reporting showed that 95% of fine art auction lots sold in 2024 were below $50,000, with the majority below $5,000.

That is not a niche detail. It is central to understanding how the market really works.

The strength of the market does not rely only on exceptional consignments. It rests on a much wider base: specialist categories, steady transaction volume, repeat bidders, repeat consignors, and the confidence buyers place in auctioneers who present stock well and build trust over time.

Online is now standard. Control is the new differentiator

This is where the digital question becomes more important.

Online bidding is no longer the point of difference. It is now standard. Buyers expect to discover, register, watch, bid and transact online without friction. They also expect more from the experience around the sale: better presentation, clearer information, stronger reassurance, and a more direct relationship with the auction house itself.

This matters even more as newer and younger buyers continue to enter through categories that sit across fine art, luxury and collectibles. Collecting habits are broadening. Digital expectations are rising. Houses are competing not just on stock and expertise, but on how confidently they bring both to market.

And yet much of the middle of the market still relies on a model that makes it harder to stand apart.

The problem with the shared model

That model made sense for a long time. Third-party bidding platforms solved real problems. They offered reach, brought in remote bidders, reduced the friction of early online adoption, and helped many auctioneers modernise faster than they otherwise could.

But they also created a kind of digital sameness.

When many houses are drawing from the same external channels, relying on the same audience pools, and offering buyers a similar marketplace-led journey, the differences between them can become less visible online than they should be.

A house may have deep expertise, a distinctive brand, and strong client service, but if its digital route to market is largely shared with its peers, it becomes harder for that uniqueness to come through in a commercially meaningful way.

That is not just a branding issue. It is a strategic one.

Because in a more mature digital market, the value no longer sits only in access to bidders. It also sits in ownership of the relationship.

Who registers directly with your business?

Who bids but does not win?

Who comes back for the next specialist sale?

Who responds to your campaigns, your catalogues, your category expertise, your tone, and your brand?

Who becomes part of your audience rather than simply passing through someone else’s ecosystem?

These are not small marketing details. They shape the long-term strength of the business.

What the tier-one houses already understand

That is the logic the tier-one houses already understand.

They are not running auctions on their own platforms simply because they are large enough to do so. They are doing it because they know that platform ownership supports commercial control. It helps them shape the buyer experience, retain more value, and build direct relationships that compound over time.

Most smaller auction houses are not Sotheby’s, Christie’s or Bonhams. But that is not really the point.

The point is that the logic is no longer reserved for the top tier.

The old excuses are getting weaker

For years, smaller and mid-sized houses could reasonably argue that taking control of their own digital route to market was too expensive, too slow, or too difficult.

That argument is becoming weaker.

Technology is moving faster. Implementation is easier. The tools available to auctioneers are more capable and more accessible than they were when many businesses first entered the online auction world.

That changes the conversation.

The question is no longer simply whether a smaller auction house can adopt a more owned digital strategy.

It is whether it can afford not to.

If the rest of the market continues to operate within a largely shared model, the gap between leaders and followers will grow. More ambitious houses will use better technology to differentiate more clearly. New entrants will spot the opportunity to build modern, owned, brand-led businesses from the outset. And those still relying too heavily on third-party structures risk becoming increasingly interchangeable.

That is the real danger.

Not that marketplace channels exist, but that too many auctioneers allow those channels to define too much of the customer relationship.

Why 2026 matters

And this matters even more in 2026.

We are moving into a world where discovery is changing quickly. Buyers and sellers are not only using traditional search engines. They are increasingly turning to AI-led tools to research markets, compare providers, and form early impressions about who appears credible, specialist, and authoritative.

That shift matters because authority compounds.

Auction houses that take control of their platform, publish under their own name, and build a stronger direct digital presence have the opportunity to strengthen trust while this next phase of discovery is still taking shape.

Those that delay risk something more serious than simply lagging behind. They risk becoming increasingly interchangeable just as the market starts rewarding the clearest specialists more decisively.

Once that advantage compounds, catching up becomes much harder.

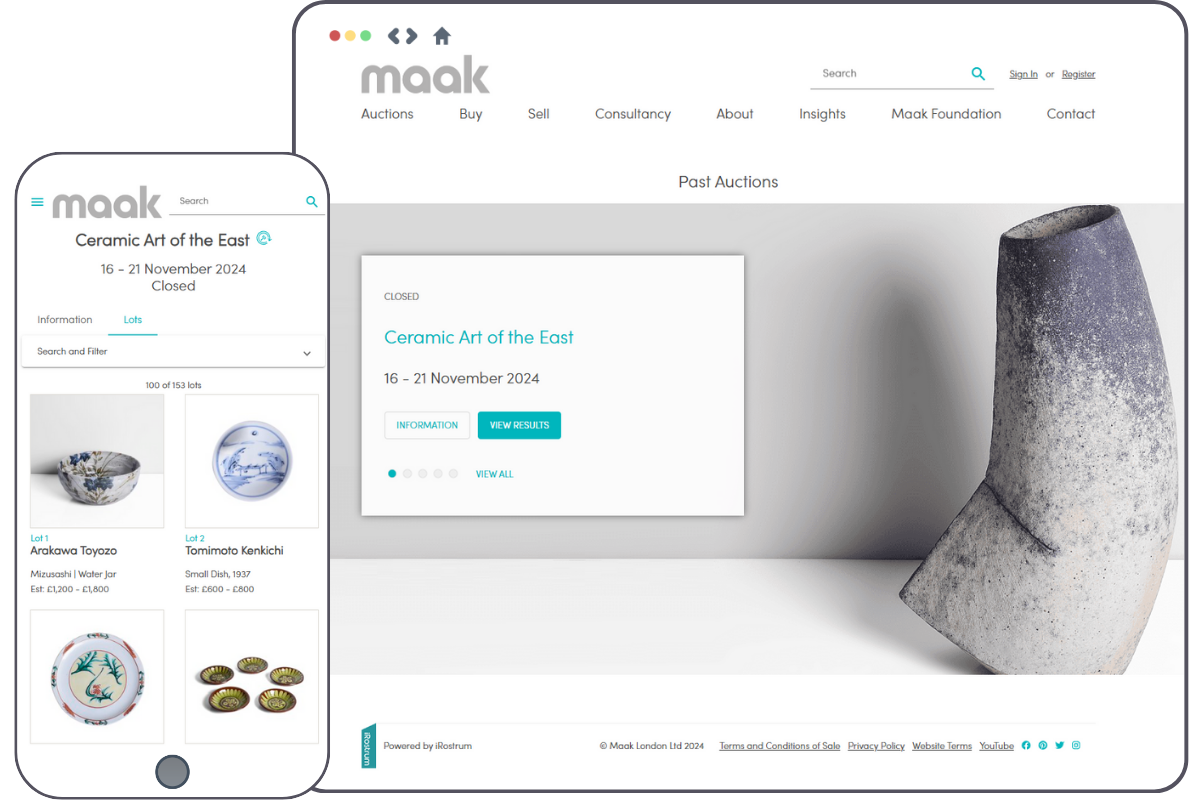

What taking control actually means

A white-label platform is one answer to that problem.

Not because it is fashionable, and not because it removes the need for external marketing, but because it gives the auctioneer a stronger foundation for building digital value under its own name. It creates more control over the bidder journey, more ownership of audience data, more freedom in presentation, and more scope to turn expertise and reputation into a repeatable commercial advantage.

This is not about abandoning every external channel. For many houses, third-party platforms will continue to play a role in visibility and discovery.

But they should be a route into the business, not the centre of it.

That is the distinction more of the market now needs to grapple with.

The real opportunity

The top tier has already decided that digital ownership matters. The technology barrier is falling. Buyer expectations are rising. Discovery is evolving. Differentiation is becoming harder inside a shared model and more valuable outside it.

In that context, auction houses that take more control of their digital route to market are likely to be the ones that define the next phase of the industry. Those that move now can build authority, strengthen trust, and create a more defensible position while the market is still taking shape.

Those that wait may not just fall behind. They may find the leaders in their category have already been decided for them.